Oops! Something went wrong while submitting the form.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

By clicking “Accept”, you agree to the storing of cookies on your device to enhance site navigation, analyze site usage, and assist in our marketing efforts. View our Privacy Policyfor more information.

2026 USA Social Security Strategies ➲ Navigating the Retirement Earnings Test

This blog article aims to help American early retirees navigate the Social Security Administration's Retirement Earnings Test if they decide to take "Early Retirement" whilst continuing to work in some capacity.

Introduction ➲ The American Working Retiree’s Paradox

For many USA professionals, 2026 marks the beginning of a sophisticated "semi-retirement."

The plan usually involves claiming Social Security benefits while transitioning into high-level consulting or advisory roles.

However, this strategy often triggers the Social Security Retirement Earnings Test (RET), a regulatory mechanism that can temporarily suspend benefits for those who have not yet reached Full Retirement Age (FRA).

In 2026, the financial stakes are precise.

For retirees under their FRA for the entire year, the exempt earnings threshold is $24,480; for every $2 earned above this, $1 in benefits is withheld.

For those reaching their FRA in 2026, the threshold increases to $65,160 for the months preceding their birthday, with a $1 withholding for every $3 in excess earnings.

While often viewed as a penalty, these rules are a navigable hurdle for the informed strategist.

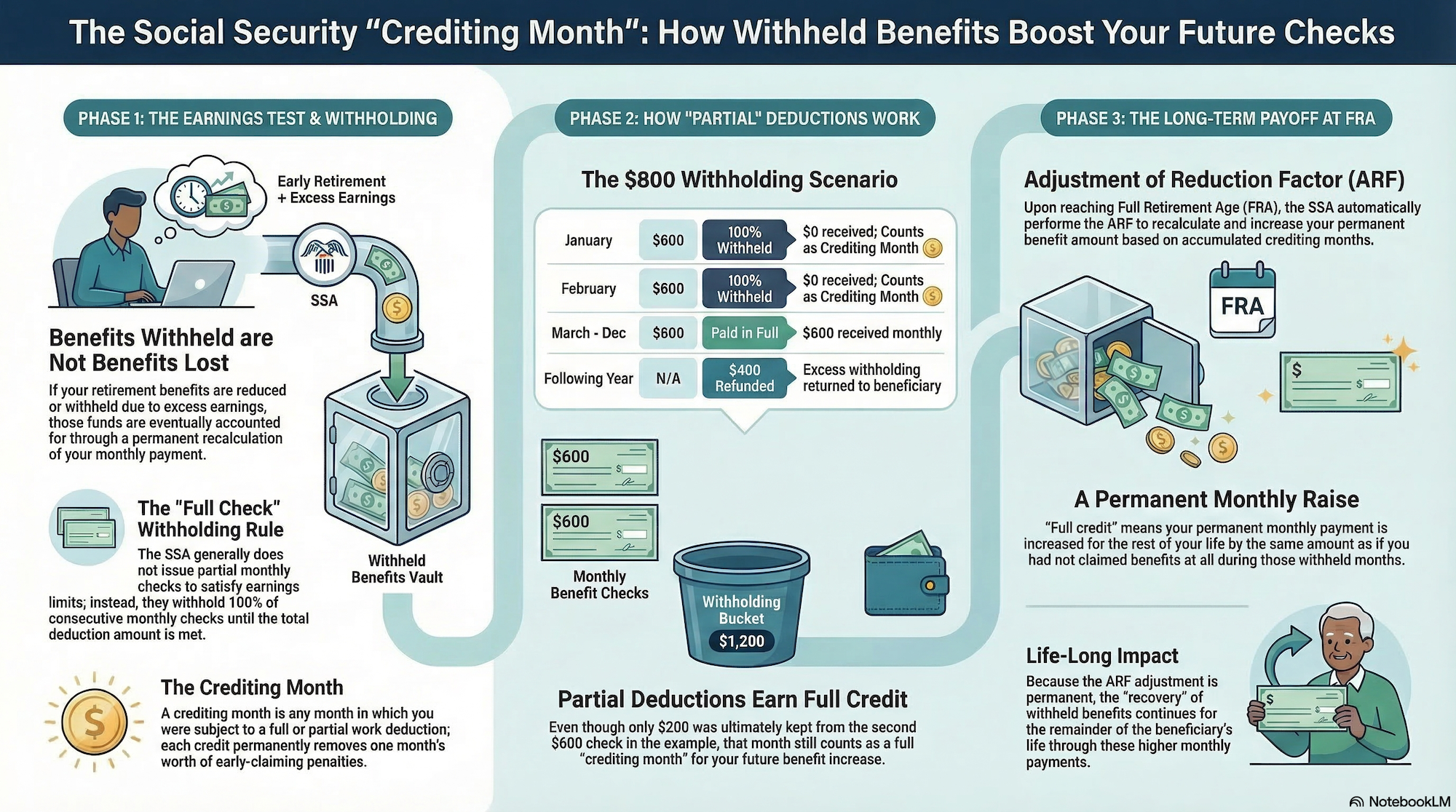

The "Ghost" Money ➲ Why Withheld Benefits Aren’t Actually Lost

A common misconception among early retirees is that withheld benefits are a "tax" that disappears into the federal ether.

In reality, the RET functions more like a "re-indexing" of your start date.

Through the Adjustment of Reduction Factor (ARF), the Social Security Administration (SSA) restores these funds by permanently increasing your monthly check once you reach your FRA.

For a high-earning consultant claiming at age 62, the initial benefit is reduced by approximately 30%.

However, if your 2026–2031 earnings are high enough to trigger a full withholding for all 60 months leading to age 67, that 30% penalty is completely erased.

Your benefit is recalculated at age 67 as if you had never claimed early, providing a significant "win" for longevity planning and a higher guaranteed income floor.

As the "Restoring Social Security Benefits" source clarifies:

"For every month your benefit was withheld, the SSA treats your record as if you had delayed your initial claim by one month."

The Charity Trap ➲ The "Fruit and Tree" Doctrine You Can't Ignore

High-earning professionals often attempt to bypass the RET by directing client payments or "gross wages" directly to a 501(c)(3) charity.

This maneuver fails due to the "Anticipatory Assignment of Income Doctrine," a legal principle establishing that income is taxable to the person who earns it.

Under the "constructive receipt" rule, the moment you perform a service, the right to that income is legally yours; gifting it away afterward does not change its status as "countable earnings."

Sophisticated retirees must distinguish between "Pre-tax" income and "Pre-RET" income.

While a donation might provide a Schedule A deduction for your IRS Form 1040, it does nothing to lower the earnings figure used by the SSA.

The SSA receives W-2 and Schedule SE data directly from the IRS through a robust data-sharing agreement, meaning gross earnings are flagged before any charitable intent is recorded.

For the SSA, the "fruit" is counted the moment it is grown on your "tree," regardless of where you eventually place the basket.

The "Grace Year" Exception

A very important exception to the above applies for a limited time during the remainder of your first year "grace year" of early retirement.

The exception applies during each month (including the month your retirement benefits commence) until December in your first year of retirement, so long as you earn less than the 2026 monthly exempt threshold of $2,040 as a W-2 employee, or work less than 15 hours a month in your own business.

For each month you are considered "retired" during your grace year, you can be paid your full retirement benefit, whilst not being concerned about your personal monthly earnings (or monthly earnings from your business that do not involve you personally, such as having a substitute cover your clients whilst you wind back your hours).

For each month Social Security considers you "retired" during your grace year, your earnings for that month (including any earnings gifted to your preferred charity) are not considered for withholding by Social Security.

Due to the significant benefits that can accrue under the "Grace Year" exception, if you turn 62 or plan to stop or reduce your working hours late in the year, we recommend you seriously weigh the advantages and disadvantages of retiring immediately, versus waiting until January or another month early in the following year so that you can maximize the number of months that you are eligible to take advantage of within your "grace" year.

For example: If it happens that you will turn 62 in October, or currently plan to stop work and start early retirement in December, you would only have 1 month (ie., December) where you are "Grace Year" eligible, whereas deciding to delay starting your retirement until January the following year would give you 12 months of "Grace Year" eligibility!

Important: It is critical that you seek expert Attorney advice regarding what is considered to be "working" as this is defined very broadly and is not just the hours you spend directly serving clients. If you get this wrong, someone could report you and you could be investigated by Social Security, and charged with fraud against the Federal Government.

The "Substantial Services" Paradox ➲ Working When You Earn $0

For highly skilled professionals—such as doctors, lawyers, and management consultants—the SSA looks beyond the paycheck via the "Substantial Services" test.

Even if you structure your business to show $0 in monthly profit, you can still be found "not retired" if you provide significant value to an enterprise.

The SSA evaluates "mental effort" and "business contacts" as devoted time, even if those hours aren't billed to a client.

The thresholds for this test are strictly enforced under POMS RS 02505.065:

Less than 15 hours: Generally considered retired.

15 to 45 hours: Potentially "substantial" if the individual is in a highly skilled occupation.

More than 45 hours: Almost always considered substantial services.

The "Highly Skilled Occupation" clause is particularly demanding.

According to CFR § 404.447, the SSA considers the "technical and management needs of the business" as a primary factor.

If you are a consultant maintaining business contacts, advising on long-term strategy, or planning operations, you may trigger a benefit withholding even if your billable hours remain low.

An Important Reporting Requirementfor International Travel

Even though this work is covered by U.S. taxes and the standard 15-hour rule protects the monthly checks, the SSA still maintains strict reporting rules for international travel.

If you are younger than your Full Retirement Age at any time during the year, you are strictly required to notify the SSA if you are working outside the United States.

Therefore, the retiree must still contact the SSA to report their overseas work arrangement, even if their hours are minimal

Correction: Year 2 Onwards [Annual Easonigs Limit] = "Annual Earnings Limit" - AI Generation Typo Error.

The "Grace Year" Escape Hatch

If you are planning a mid-year exit from a high-earning corporate role, the "Special Rule" (Monthly Earnings Test) is your primary escape hatch.

This rule allows you to receive a full Social Security check for any month the SSA considers you "retired," regardless of how much you earned earlier in the year.

For 2026, the monthly exempt threshold is $2,040.

This rule allows an executive to earn a seven-figure salary in January and February, retire in March, and still collect a full benefit for the rest of the year.

However, self-employed consultants must tread carefully: to qualify for a "grace month," you must pass the "substantial services" test for that specific month.

You cannot simply take a $0 draw in March if you worked 50 hours closing a legacy deal.

As the SSA documentation notes:

"The SSA counts what you do after you claim, not just the annual total in that first year."

The January Strategy: Maximising Social Security Grace Years

By delaying the start of your retirement to January of the year after you turn 62, that entire new calendar year becomes your one-time "grace year".

Here is how this strategy benefits you:

1. A Full 12 Months of Protection

The Social Security Administration's (SSA) Special Earnings Limit Rule can only be used for one year (usually the first year of retirement).

Under this rule, the SSA will pay a full Social Security check for any whole month you are considered retired, completely regardless of your total yearly earnings.

By starting benefits in January, you maximize this rule, giving you 12 full months where the monthly test overrides the strict annual earnings limit.

2. Maximizing the Substitute Worker Strategy

If you are self-employed and use this January start date in combination with the substitute worker strategy, the financial payoff is significant.

As long as you avoid performing "substantial services" by keeping your personal involvement under 15 hours a month for the entire year, the SSA will consider you "retired" for all 12 months.

This means you will receive all 12 of your unreduced Social Security checks for that year, completely regardless of how much massive net profit the substitute worker generates for the business.

The highly profitable business earnings will not trigger the standard 1−for−2 withholding penalty during this 12-month period.

3. You Choose When to Apply

The SSA allows you to decide exactly when to apply based on what works best for your financial situation.

You can apply up to four months before you want your retirement benefits to actually start.

So, to secure a January start date, the retiree could submit their application as early as September or October of the prior year.

The Following Year

It is important to plan ahead, because this protection is strictly a one-year provision.

Beginning in January of their second year of retirement, the grace year is over.

From that point onward, the monthly test disappears, and any high net profits generated by the business will be measured directly against the standard Annual Earnings Test, which will cause your future benefits to be withheld

HSA Myths ➲ Why Your Health Savings Won't Save Your Benefits

Health Savings Accounts (HSAs) are often marketed as the ultimate triple-tax-advantaged tool, but they offer no relief from the Retirement Earnings Test.

A common myth is that contributing to an HSA lowers "earned income" for SSA purposes.

While these contributions are "FICA-exempt"—meaning both you and your employer save on payroll taxes—they remain "RET-visible."

The SSA defines wages as the gross amount before any employer deductions for insurance or savings plans.

While your HSA contribution lowers your taxable income on your IRS 1040, the "gross wages" reported to the SSA remain un-reduced.

For the RET, your earnings are calculated based on the total value of your work effort, making HSAs an excellent tax tool but an invisible factor in Social Security withholding calculations.

Conclusion ➲ The Long Game of Retirement in the USA

Sophisticated 2026 planning demands a shift from immediate liquidity to long-term benefit floor-raising.

Continued work should be viewed as an investment; every month of withheld benefits results in a permanent upward adjustment at your Full Retirement Age via the ARF.

Furthermore, a high-earning year in 2026 can replace a lower-earning year from your early career, potentially raising your 35-year earnings average and your baseline benefit.

As you finalize your retirement strategy, the technical nuances of the RET should not discourage you from professional activity.

Instead, they should inform how you structure your time and income recognition.

The fundamental question for early retirees is no longer how to avoid Social Security withholding excess earnings, but how to optimize for tomorrow's higher benefit ceiling.

Full disclosure: The first draft of this blog article and the cover image infographic were AI-generated.

This blog article is intended for general interest + information only.

To the extent this article is deemed advertising or solicitation, it is hereby identified as such.

It is not intended to constitute legal advice; the statements made are opinions about general situations, and they are not a substitute for advice as to any specific matter.

We recommend you always consult a lawyer for legal advice specifically tailored to your needs & circumstances.

Share + Subscribe

RSS link copied!

Thank you! Please check your email to confirm your subscription.

Oops! Something went wrong. Please check your email and try again.

Share

Subscribe

COmments

No items found.

Post a comment

Thank you!

Your comment has been received and we will approve it shortly.

Your comment has been received and we will approve it shortly.